Something hit my windshield on the highway last week. A small rock. No big deal, right?

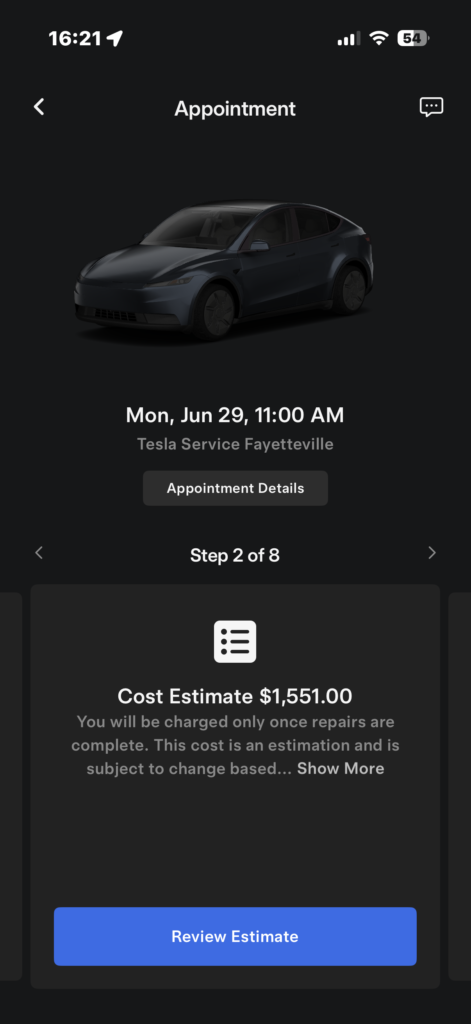

Wrong. The repair estimate for my Tesla windshield came back at $1,551. No warning, no time to prepare. Just a bill sitting in my inbox on a Tuesday afternoon.

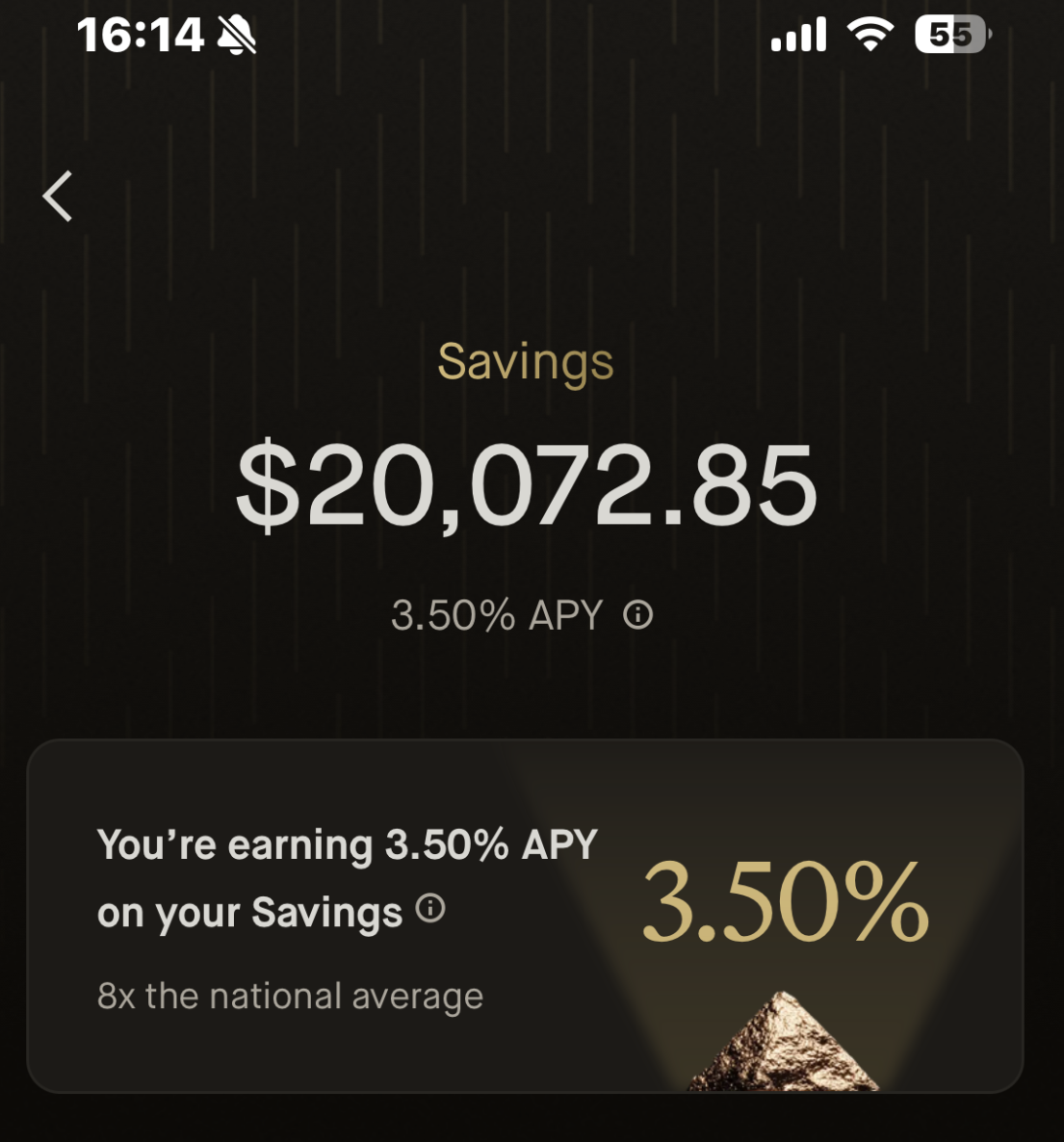

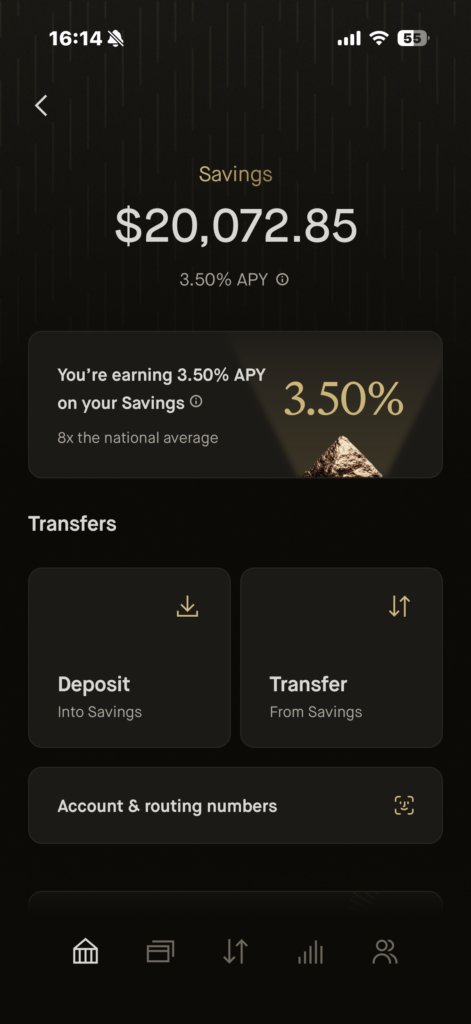

That moment reminded me of something I tell every Korean friend who moves to the US: this country will surprise you financially, and it will surprise you often. I’ve been keeping a personal minimum of $20,000 in cash as my emergency fund for years. Not because some financial book told me to. Because life in America taught me the hard way.

Table of Contents

- What Is an Emergency Fund?

- Why the US Is Full of Financial Surprises

- How Much Should You Actually Save?

- Where to Keep Your Emergency Fund

- How to Start Building It

- Common Mistakes People Make

- FAQs

What Is an Emergency Fund?

An emergency fund is cash you keep saved for unexpected situations. Not for vacations. Not for a new phone. Only for real emergencies.

Think of it as your financial floor. The lowest point you’ll let yourself fall to. No matter what happens — a job loss, a car accident, a hospital visit — this money is there to catch you.

Financial experts call it a “liquid” fund. That just means it’s easy to access quickly. No selling stocks, no waiting days for a wire transfer. Just money sitting in an account, ready when you need it.

Why the US Is Full of Financial Surprises

Here’s something nobody told me before I moved here.

In Korea, a lot of costs are predictable. Healthcare is cheaper. Public transportation is everywhere. You can get by without a car in most cities. But in the US? Almost everything costs more than you expect — and the surprises come out of nowhere.

Here’s what I mean:

- My Tesla windshield cracked from a small rock on the highway. Replacement cost: $1,550. Insurance covered part of it, but I still owed a big chunk.

- A friend of mine called an ambulance after a bad fall. He assumed insurance would cover it. The bill came back at over $3,000 after insurance.

- Property taxes, car registration fees, HOA fees, utility deposits when you first move in — these smaller costs add up every single month.

In Korea, I never had to think about most of these things. Here, they’re just normal life.

The scary part is how many people say to themselves: “That won’t happen to me.” I said the same thing. Until it did. Living in the US without an emergency fund isn’t just risky. It’s playing a game where you only lose.

How Much Should You Actually Save?

Most financial experts say 3 to 6 months of your living expenses. That’s the standard advice. But I think that’s the floor, not the goal.

3 months of expenses

The bare minimum. If you lost your job tomorrow, you’d have some time to breathe. But not much.

6 months of expenses

Much safer. Especially if you’re an immigrant with no family safety net nearby. If something goes wrong, you have real time to figure things out without panic.

My personal rule: $20,000 minimum, always

I keep at least $20,000 in cash at all times. No exceptions. This isn’t about following a formula. It’s about peace of mind. When my windshield broke, I didn’t panic. I just paid it and moved on. That feeling is worth more than any investment return I could have gotten on that money.

If $20,000 feels far away right now, that’s completely okay. Start with $1,000. Then $3,000. Then keep building. The number matters less than the habit of getting there.

Where to Keep Your Emergency Fund

This is a question I get a lot. Here’s the simple answer.

A high-yield savings account (HYSA). That’s it. A regular savings account at most big banks earns almost nothing — sometimes 0.01% interest per year. A high-yield savings account earns much more. Right now, many online banks are offering around 4% to 5% APY — that’s the yearly interest rate on your money.

Some solid options:

- Marcus by Goldman Sachs

- Ally Bank

- SoFi Bank

All of these are FDIC insured. That means if the bank ever has problems, the US government protects your money up to $250,000.

Do not put your emergency fund in:

- The stock market — it can drop 30% right when you need the money most

- A CD or fixed deposit — you usually can’t access it quickly without a penalty

- Your regular checking account — it’s too easy to spend without thinking

How to Start Building It (Even When Money Is Tight)

I know what you’re thinking. “I can barely cover rent. How am I supposed to save $20,000?” Here’s what actually worked for me:

- Treat it like a bill. Every paycheck, move a set amount to your emergency fund before you spend anything else. Even $100 a month adds up to $1,200 a year.

- Start small and stay consistent. Don’t try to save $500 a month if that’s not realistic. Save $50 every month without fail. Consistency beats big numbers.

- Use windfalls. Tax refunds, work bonuses, cash gifts — put a big portion straight into your emergency fund until you hit your goal.

- Keep it separate. Open your HYSA at a different bank from your regular account. Out of sight really does mean out of mind. It’s harder to spend money you don’t see every day.

Common Mistakes People Make

Investing before building an emergency fund

I’ve seen this happen so many times. Someone puts $5,000 into stocks, then their car breaks down and they have no cash. They end up selling their investments at a loss just to cover the repair. Don’t let that be you. Emergency fund first. Always.

Thinking “I’ll do it when I have extra money”

There will never be a perfect time. Extra money always finds somewhere to go. You have to decide that the emergency fund comes first — not when it’s convenient, but right now.

Using it for non-emergencies

A sale at the mall is not an emergency. A new gadget is not an emergency. Save it for situations that would seriously hurt you financially if you didn’t have the cash.

Never updating the amount

Your expenses change over time. If your rent goes up or your family grows, your emergency fund target should grow too. Check it once a year.

FAQs

Should I pay off debt first or build an emergency fund?

Do both at the same time, but start small. Build a $1,000 emergency fund first, then attack high-interest debt hard. Once your debt is under control, build the full fund.

What counts as a real emergency?

Job loss, medical bills, urgent car repairs you need for work, a broken appliance you can’t live without. A flight deal or a shopping sale doesn’t count.

What if I have to use part of my emergency fund?

Use it — that’s exactly what it’s for. Then start rebuilding it right away. No guilt. That’s the whole point of having it.

Is $20,000 too much to keep in cash?

Some people will say you could invest that money and earn more. Maybe. But when that $1,550 windshield bill showed up, I didn’t have to stress or scramble. I just paid it. That kind of calm has real value.

Do I really need a separate bank account for this?

Yes. Keep it at a different bank from your everyday spending account. If it’s too easy to reach, it’s too easy to spend.

You Can’t Build Anything Without a Foundation

Every financial goal — buying a house, building investments, retiring early — needs a strong base underneath it. Your emergency fund is that base.

Don’t skip it. Don’t delay it. Don’t wait until things “settle down.” In the US, things don’t settle down. Life keeps moving, and the surprises keep coming.

Get your emergency fund in place first. Then build everything else on top of it. That’s not just my opinion — every financial expert will tell you the same thing. This is step one. Always.